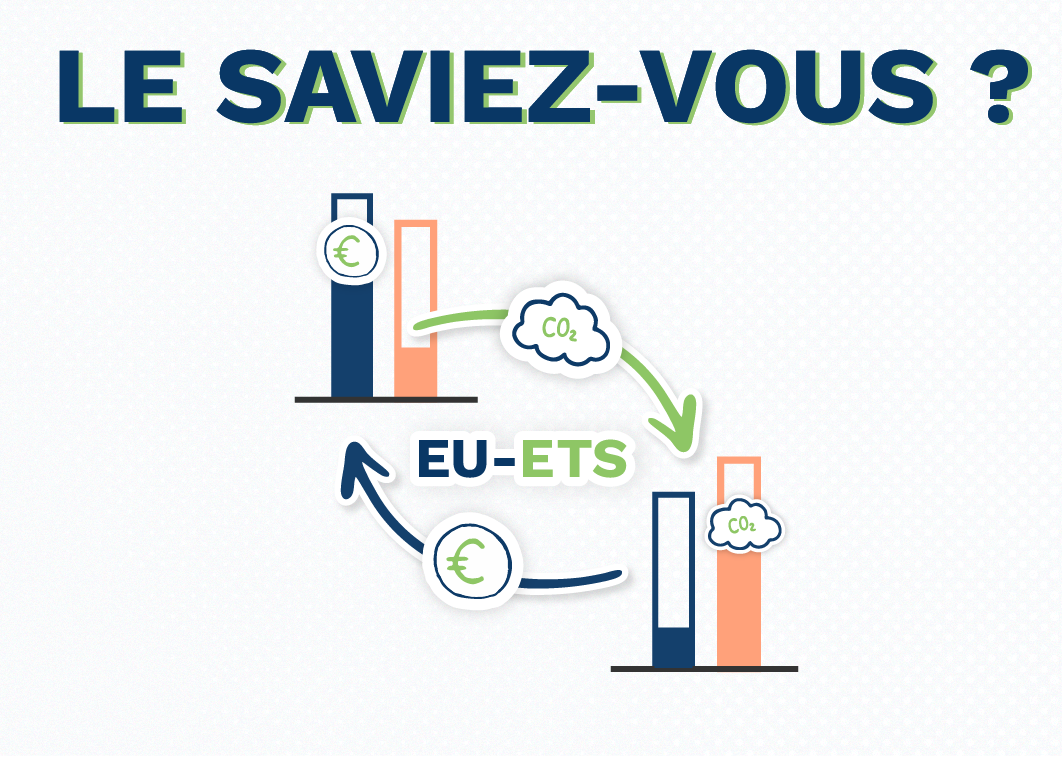

A carbon market based on the polluter-pays principle

As part of its decarbonization drive, the EU adopted the Emissions Trading System (EU ETS) in 2005. The principle is simple: make the main emitters of greenhouse gases pay to encourage them to reduce their emissions.

The scheme applies to the industries with the highest emissions, in particular power generation, energy-intensive industry (oil refining, steel, paper, glass and cement production), commercial aviation for routes within Europe and, since 2024, maritime transport (routes within the EU and departure and/or arrival in a European port). All EU states are concerned, as well as Iceland, Norway, the UK and Switzerland.

70€/ton

Spot price ofCO2 in June 2024

Source: European Commission

In practical terms, industries subject to the EU ETS must purchase emission allowances at auction corresponding to their actual emissions, or face a fine. Quotas are also allocated free of charge to certain sectors. The players concerned also have the option of trading allowances among themselves, via an exchange. This is known as the EuropeanCO2 market.

How the EU ETS works

The EU ETS covers around 40% of EU emissions, and almost 10,000 installations are subject to it. In France, 1,059 installations are covered by the scheme, with emissions of around 80 MtCO2 (2022 data).

In May 2023, Europe adopted a reform of the mechanism. Its aim: to tighten the terms of the system in line with the EU’s ambition to reduce greenhouse gas emissions by 55% by 2030 (compared with 1990). One of the challenges of the reform is to broaden the sectors covered by the scheme. It provides for the building and road transport sectors (and others not covered by the current mechanism) to join a separate scheme, commonly known as EU ETS 2, from 2025, with an adaptation phase of around two years. After this period, EU ETS 2 should be fully operational and allow trading in allowances.

For players already subject to the EU ETS, i.e. manufacturers, the reform contains changes with far-reaching consequences. Three measures will have a major impact in the medium term:

- Reducing the number of quotas put into circulation each year.

- The end of free emissions quotas.

- The Border Carbon Adjustment Mechanism (BCAM).

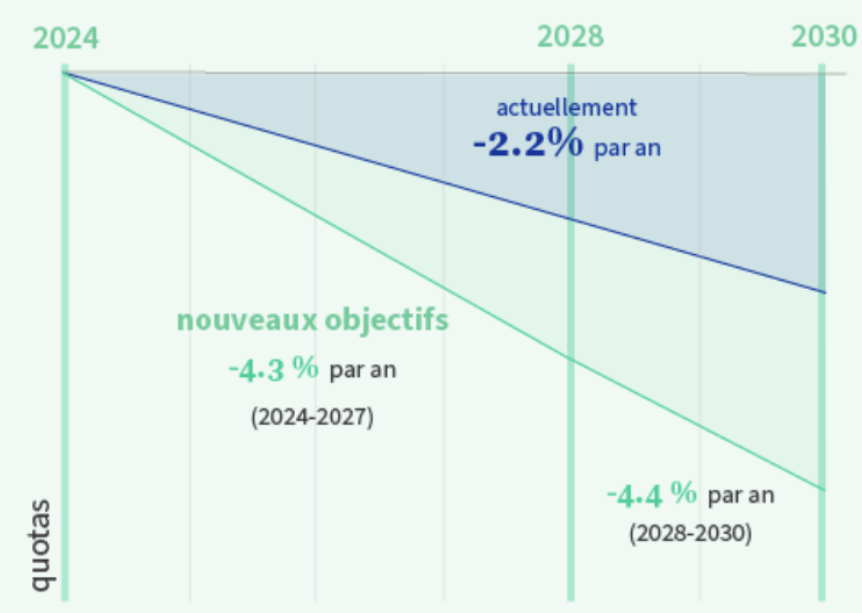

The sharp reduction in the number of quotas issued each year

Rights to pollute are regularly auctioned by European countries. The number of allowances put on the market each year is decreasing in line with European decarbonization targets. Since 2021, the annual reduction rate has been 2.2%. As part of the reform of the system, this annual reduction rate has been increased to 4.3% from 2024 to 2027 and to 4.4% from 2028 to 2030, i.e. a doubling of the rate initially planned.

Evolution of the reduction in the number of quotas

The reform of the EU ETS mechanism is aimed at earmarking 100% of auction revenues for climate-related expenditure (e.g. energy renovation).

2.1 billion euros

Revenues generated by the sale of allowances in France in 2023

Source: French Ministry of Ecological Transition

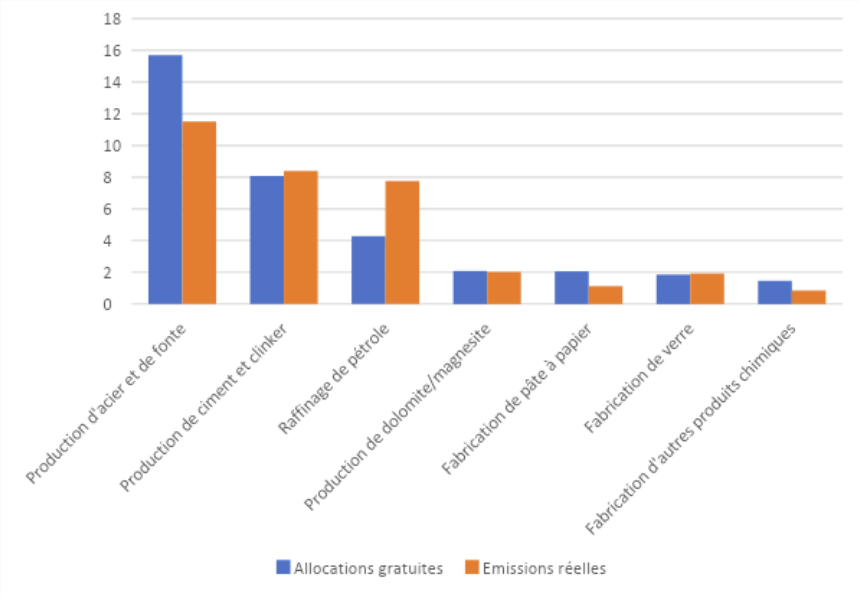

The end of free quotas

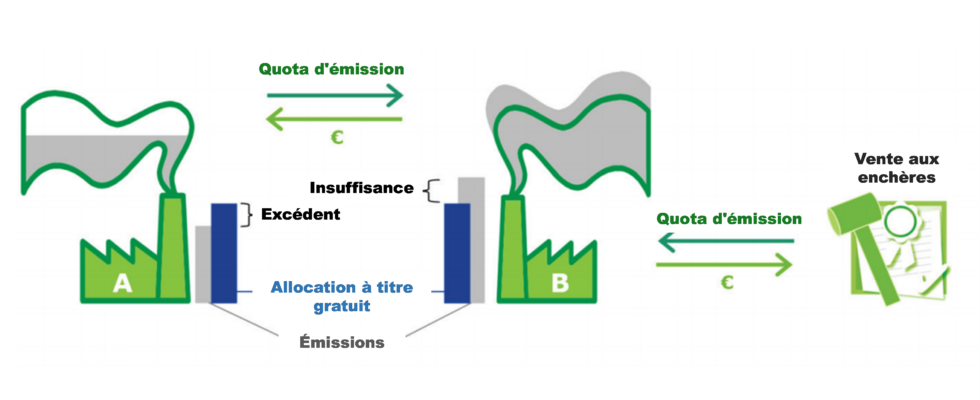

A significant proportion of the allowances are allocated free of charge to industries at risk of carbon leakage, or, according to the European Parliament, the relocation of greenhouse gas-emitting industries outside the EU to avoid stricter standards. The temptation to relocate production in order to remain competitive can be great.

In 2023, free allocation concerned almost half of the allowances issued in Europe. Only electricity production does not benefit from free quotas. Over sixty sectors and sub-sectors are eligible. The EU wants to put an end to these free allocations of allowances, which account for the vast majority of emissions, or even more depending on the year and the industrial sector.

Free allocations of emission allowances and actual emissions from the main sectors concerned in 2023 (in millions of tonnes ofCO2 equivalent)

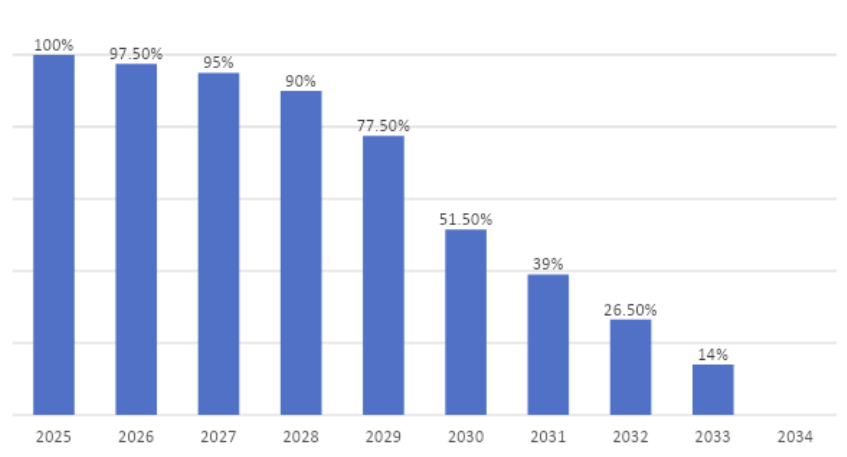

Free quotas will be phased out from 2026, to give manufacturers time to adapt. The process will last until 2034. Depending on the sector (and on the price ofCO2 at that time), this change will result in a greater or lesser increase in production costs.

MACF for fair competition

In parallel with the end of free allowance allocations, the Border Carbon Adjustment Mechanism (BCAM) will gradually be implemented. This mechanism aims to preserve the competitiveness of European industry by applying a CO2 price to products imported from non-EU countries, based on their carbon content. If a CO2 price already exists in the exporting country, only the difference between it and the CO2 price in Europe will have to be compensated.

Initially, to limit the complexity of the mechanism, the MACF will only apply to a limited list of products: steel, cement, aluminum, nitrogen fertilizers and hydrogen. The production of these goods accounts for around half of the EU’s industrial emissions. Electricity production is also concerned.

Implementation is gradual, with an initial transition period starting on October 1, 2023 and ending on December 31, 2025. During this phase, companies importing the targeted products must declare the volume of their imports and the greenhouse gas emissions linked to their production. This transitional period should enable stakeholders (importers, producers and authorities) to familiarize themselves with the scheme and fine-tune its modalities.

From 2026, the period of effective operation will begin. Importers of the targeted goods will then be required to purchase MACF certificates at the average price determined on the quota market. Initially, only a fraction of the emissions from imported products will have to be covered by the purchase of MACF certificates. This proportion will increase until it reaches 100% in 2034. The rate of increase corresponds to the rate at which free quotas are phased out. The two measures are closely linked, so that manufacturers located in Europe who no longer benefit from free allowances can maintain their competitiveness against imports of competing products.

Scheduled reduction in free emission quotas for sectors covered by the MACF

The reduction in the number of emission allowances allocated free of charge, and therefore conversely the proportion of imports requiring the acquisition of MACF certificates, will accelerate throughout the second phase of the scheme.

To avoid the growing burden of carbon constraints, manufacturers have only one option: decarbonize their processes.